Comments

Comments from June 19, 2026.

The main chatter in the South over the last week has been the unfortunate news of several well-known hardwood sawmills closing their doors. The mills are located across the region and owned by highly respected market participants. Some have already cut their last log, while others are due to turn off the lights later this summer.

Given the ongoing issues with sluggish domestic demand for grade lumber, the downturn in crosstie buying, and the high costs of freight and keeping a sawmill running, the closures do not come as a big surprise. One sawmill owner said he was mothballing his mill, but “only because it would be a horrible time to go to auction right now.”

The hardwood trade remains a challenge for those still operating. One sawmill contact in Alabama said he was down to 60% production over the last six weeks, bemoaning the continuing impact of high diesel prices. A lack of logs has been an issue in both his state and Mississippi, as loggers increasingly chase hardwood pulpwood and Southern Yellow Pine, leaving hardwood mills with few options. “No matter how much supply seems to diminish, demand diminishes too,” the contact said. “You wonder where we’ll find the bottom.”

ASH: The market for green Ash is evenly balanced, with no price changes this week. In contrast, there are plenty of changes to published prices for dry stock. International interest drives increases to the 4/4 #1C listings as well as the listings and ranges for 4/4 #2A. Southern exporters have noticed cooling demand for other kiln dried Ash items, however. Reported prices drive reductions to the listings and noted ranges for 4/4 Fas, 8/4 #1C, and 8/4 #2A. With the heat of the Southern summer well underway, loggers are encountering few issues when harvesting lowland species like Ash.

#2A&3A OAK: Markets for green #2A&3A Oak are performing much like they have all spring. In most areas, Oak logs are readily available for sawmills that want them, resulting in ample lumber supplies for flooring factories. Most residential flooring plants are not buying in big volumes, though sawmill operators view higher demand from truck trailer flooring plants as a positive sign. Still, one contact said significant demand improvement for #2A&3A Oak “feels a long way off.” Prices in observed business keep all the #2A&3A Red Oak and White Oak listings intact.

RED OAK: Several sales contacts indicate kiln dried 4/4 #1C Red Oak remains popular, particularly in overseas markets. Reported prices bear out this sentiment, with the listings advancing this week. Thanks to international interest, kiln dried 4/4 Fas also receives a bump, with the listings and ranges all moving up. The market for green Red Oak is flat, with supply and demand evenly matched and prices holding steady.

WHITE OAK: As has been the case for a couple of months, White Oak is a tough species to move in the South. On the green side, the 5/4 Fas&1f listings once again register sizeable reductions, while all #1C items, 4/4 through 8/4, also drop. Kiln dried markets are not strong, but prices have shown less deterioration this week. Decreases to the 4/4 Fas listings are the only price changes.

PECAN & HICKORY: Southern flooring plants continue to buy Hickory, following a similar trend in the Appalachian region. Prices in observed business drive increases to all green 4/4 through 8/4 #2B&Btr listings for a second straight week.

POPLAR: International demand for Southern kiln dried Poplar remains decent overall, including Vietnamese interest in #1C and #2A. Meanwhile, Fas is moving steadily to domestic distribution yards and end users. Prices in observed business necessitate increases to the listings and low ends of the ranges for 6/4 and 8/4 Fas, along with certain 4/4 Fas and 4/4 #2A range numbers. However, the 8/4 #1C and 5/4 #2A listings and noted ranges retreat. Markets for green Poplar are more settled, though the 4/4 and 5/4 #1C listings notch modest gains.

FRAMESTOCK, CANTS, TIES, & BOARD ROAD: Upholstered furniture manufacturers are buying hardwood framestock at a steady pace, but after recent increases to the Oak and Mixed Species framestock ranges, there are no additional changes this week. Reported prices also allow the listing and range for board road to stand.

There is plenty of energy in the hardwood pallet cant business in both the Northern and Appalachian regions, but that has yet to show up in the South. The cant listing and range are unchanged in this edition. Crosstie quotas remain in effect on both sides of the Mississippi, which keep prices low but unmoved.

Comments from June 19, 2026

Surveys of Appalachian sawmills this week indicate log supplies are level to slightly lower, while green lumber sales are flat to slower. Reports of kiln dried lumber sales are split equally between slow, fair, and good. Collectively, these responses reflect the “mixed bag” and “nothing too exciting” descriptions contacts have of current market conditions. Some lumber sellers report no issues getting their asking prices, while others are adjusting them as needed to keep production moving. Relatively few changes to the Appalachian price matrices indicate supply and demand are generally aligned. For items where imbalances exist, information lifts more figures than it lowers this week.

ASH: The marketplace is readily absorbing developing green Ash at prices centered on the #2A&Btr listings in all thicknesses. Demand for kiln dried Ash is fair, with contacts reporting steady shipments to regular customers, mainly in Asia and Europe. Exports to most Middle Eastern destinations are on hold. Observed and reported prices hold all kiln dried figures steady.

BASSWOOD: Area sawmills are not cutting much Basswood, instead focusing on species that move in larger volumes. Supply shortages relative to limited demand drive gains to the kiln dried 4/4 #2A&Btr and 5/4 #1C&Btr Basswood listings and most ranges.

BEECH: This species is not heavily produced in the Appalachian region, but there is modest ongoing demand. Information shows supply-driven price pressures that lift the green 4/4 #1C&Btr Beech listings.

CHERRY: Sawmill operations are moving green Cherry production with relative ease to concentration yards that are working to bolster in-process inventories for export to China. Energy is strongest for Fas&1f in the North Central area, and all 4/4 through 8/4 listings advance. Most dry-side changes also occur in the North Central, with reports warranting increases to the 5/4 #1C listings and all 4/4 and 5/4 #2A figures. The only changes in the Appalachian region raise the listings for 5/4 Fas.

HICKORY: Despite warming temperatures, residential flooring manufacturers—responding to brisk sales of Hickory flooring—issued 5% to 10% more purchase orders for green Hickory in June than in May. Meanwhile, kiln dried 4/4 Hickory is moving well in all grades. Upward price pressure is only evident for green 4/4 Fas&1f this week, however, and the listings edge higher.

HARD MAPLE: Demand for Hard Maple has slowed, which is reflected in a negative shift in comments from market participants. One producer noted inventory growth because his kiln dried sales have “fallen off a cliff.” Another described kiln dried Fas as nearly unsellable. Declines in prior weeks have all the kiln dried figures in order in both color sorts. The impact of production declines amid low demand is evident in reported green 5/4 Fas&1f prices, with the #1&2 White and Unselected listings both rising.

SOFT MAPLE: This species has been the stronger of the two Maples, but the gap is closing amid lower interest in Soft Maple. Contacts point out softening markets for green 4/4 Fas&1f, in particular, and the listings are lowered for each color sort. Downward pressure is similarly evident in kiln dried 4/4 Fas prices, prompting reductions to the listings and low-end ranges in each color classification. The low-end ranges for 8/4 Fas also retreat in both color designations.

#2A&3A OAK: Overall lumber purchases by truck trailer flooring manufacturers have increased in June, on the strength of somewhat higher demand for finished goods. This upturn is offsetting static purchasing activity by some residential flooring plants and notably slower buying for others. Purchasing trends in June are similar for Red Oak and White Oak. No changes are required to any #2A&3A or #2A Alone Red Oak or White Oak listing.

RED OAK: Decent volumes of Red Oak logs and lumber are moving through the supply stream. Green production is mostly adequate for the market’s needs. Pricing data obtained this week warrant small bumps to the 6/4 Fas&1f listings and an equally small reduction for 8/4 #1C. Markets for kiln dried Red Oak are decent and slightly better for #1C&Btr than for #2A, though #2A still moves. Transactions for kiln dried 4/4 Fas show an upward bias that raises the listings $30 in this edition. Reported prices for other Red Oak items land at or near the listings or within the published ranges.

WHITE OAK: One producer reports no issues getting his list price for kiln dried 4/4 Fas White Oak, which is near the high end of the published range. “I also have several purchase orders for 8/4 Fas, and I’m able to move a few packs of 8-foot uppers with every order,” he said. Overall, the large spreads between the highest and lowest reported kiln dried Fas prices are reflective of a market that has been oversupplied amid reasonably steady demand. Price reductions have been necessary to generate interest in a competitive marketplace, but the magnitude of reductions has been considerably larger for some producers than others. Signs that supply and demand for most White Oak items are nearing equilibrium continue. The only changes this week lower the high-end ranges for 8/4 Fas.

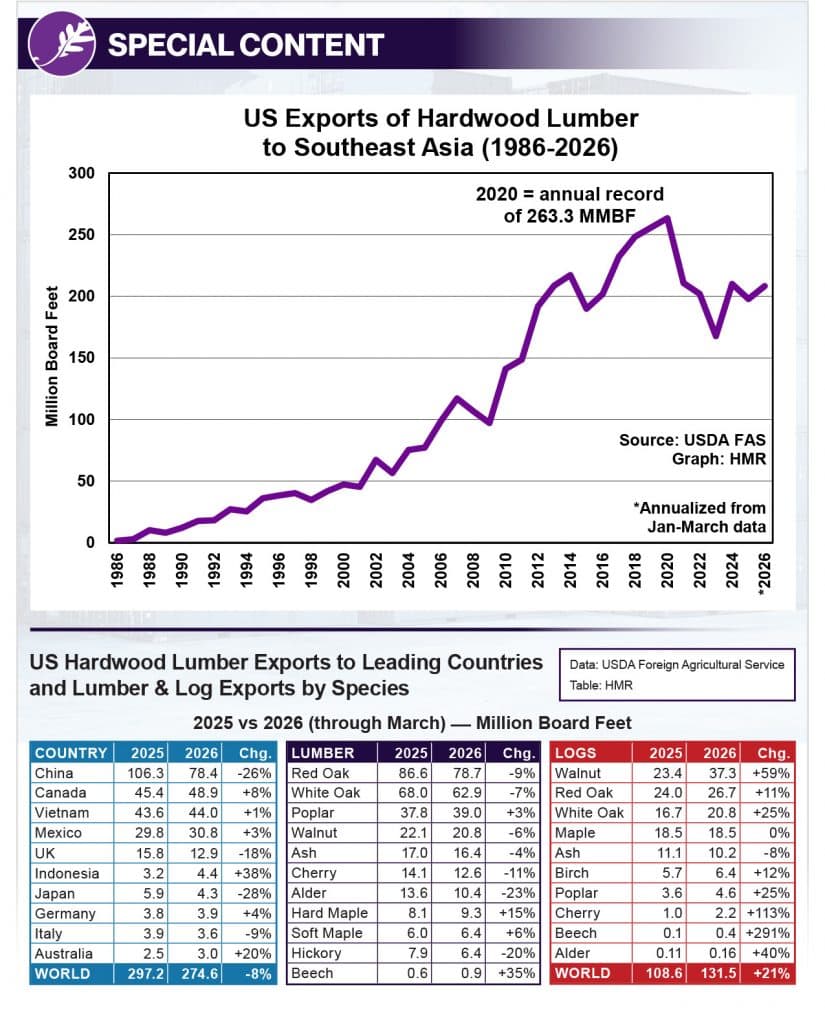

POPLAR: Domestic demand for Poplar is mostly steady, led by the moulding/millwork sector. The #1C&Btr grades also move well to distribution yards that, in turn, are having no issues moving them to their customers. Shipments of Poplar to Vietnam, which are heavy to #1C and #2A, climbed 28% year over year through April. However, Poplar exports to China fell 38% year over year through April. This after a 47% year-over-year decline during the same stretch in 2025 relative to 2024, due to the combined impact of the US-China tariff fight and faltering Chinese housing market. Poplar lumber availability increased in May, with ample log supplies spurring production. Markets struggled to absorb the additional output, prompting erosion in Fas&1f prices across most thicknesses. Supply and demand are now more closely aligned. All the green listings are unchanged this week, and the only kiln dried changes widen the ranges for 6/4 #1C.

WALNUT: Monthly US exports of Walnut logs trended sharply higher the first four months of 2026, setting records for each respective month and culminating in a one-month record of 17.6 million board feet (MMBF) in April. Official data erroneously show exports of nearly 46 MMBF in January 1981, which is exponentially higher than any month in that period. Domestic demand for Walnut lumber is steady, as is interest from Chinese buyers, whereas shipments to Canada and Vietnam have registered sizeable gains this year. Prices in observed business keep all the green and kiln dried listings and ranges in check.

FRAMESTOCK, CANTS, TIES, & BOARD ROAD: Solid hardwood framestock continues to face headwinds amid the prevalence of sheet goods in upholstered furniture. Limited framestock production aligns with limited demand, keeping the ranges for framestock intact.

Demand for cants is decent from the pallet sector. Reported cant prices show upward momentum, even from certain buyers whose purchase prices rarely budge. This suggests stronger competition from other industrial markets, or reduced production at sawmills still operating and several that have ceased operations. The latter explanation is more feasible than the former. Information is sufficient to raise the cant listing and range.

Contacts report flat-to-slower demand for crossties. Treaters are approaching purchases cautiously, as most have larger-than-desired inventories and lackluster black tie sales. No changes are warranted to the ranges.

Board road markets don’t have much energy in the Appalachian region, compared with reports of decent or improving demand in the Northern and Southern regions, due partly to usage during the construction of new data centers. While data center construction is planned in some states within the Appalachian lumber producing region, most new data centers under various stages of construction are occurring in the South, Midwest, and West, according to the Pew Research Center.

Comments from June 19, 2026.

Excess supply continues to weigh on prices for Soft Maple this week, maintaining the downward trend that began a month ago. Meanwhile, many green Hard Maple listings turn red this week amid lower reported prices from numerous market participants.

Generally speaking, Red Oak is outperforming White Oak in the marketplace. The former is moving well at steady-to-firm prices, while the latter is still working to find a floor despite increased activity in some markets the past few months.

Prices for some minor species, such as Ash and Aspen, are at relatively firm levels on the back of tight supply. On the other hand, Birch prices have slumped, as producers are struggling to move the species.

A bump in demand for pallet lumber is a bright spot for producers, with contacts describing the sector as “good” and reporting prices with an upward bias.

ASH: Tight supply caused by the spread of the Emerald Ash Borer, along with elevated export demand, are supporting Ash prices in the Northern region. A producer in the Upper Midwest described domestic supplies of Fas as “dwindling,” and said there is still a shortage of #1C in China. Broadly, prices for the species, both green and kiln dried, are at the highest levels in nearly four years. Prices rallied consistently from December 2025 through May and have since held at firm levels. The kiln dried net 4/4 Fas listing is up 9% over the past seven months. The only changes in order this week are slight bumps to the kiln dried 4/4 #2A listings.

ASPEN: Aspen prices have appreciated significantly since early 2025, including an especially sharp upturn in the first quarter of this year. Industry contacts attribute the gains to reduced production rather than higher demand. The green and kiln dried listings and ranges have registered more incremental increases since April and are unchanged this week. A sawmill in Michigan that still produces the species recently reported an increase in inquiries for kiln dried Fas and #1C.

BASSWOOD: No producers in the Northern region have listed Basswood among their bestsellers in recent weeks. Listings and ranges for the species are again unchanged this week amid consistent reported prices. Prices have largely held steady over the past two months, following a sharp supply-driven rally in the first quarter of this year. The window blind and shutter sector is the largest domestic markets for Basswood, and ongoing economic uncertainty is working to limit demand from that sector; US new home completions were down from 2024 and 2025 levels in April, according to FRED. In a positive for producers, one exporter in Michigan reported a “significant” increase in demand for Basswood from China in June.

BIRCH: Birch is not moving well for producers in the Northern region. No market participant has listed the species as a bestseller in recent weeks, while several producers have listed it as a worst-seller. Buyer interest for #1C&Btr items is centered on Sap&Btr and Red color designations, whereas demand for Unselected material is quite limited. Observed prices are consistent with prior weeks, holding all the listings and ranges steady at depressed levels. The green 4/4 Fas listing has not posted a gain in 13 months and is down by 16% from a year ago.

HARD MAPLE: Kiln dried Hard Maple is mostly moving well for producers in the Northern region, particularly the Upper Midwest. Several items have been commonly listed among bestsellers by sales contacts in recent weeks, and all the #1&2 White and Unselected listings and range numbers are unchanged in this issue. The kiln dried listings have rallied over the past two months following sharp declines in the fourth quarter of 2025 and a fairly steady first quarter. Downward price pressure was noted in reported green prices this week, leading to decreases to all Fas&Sel listings and the 4/4 #2A listings in both color designations. Rising log supply following mud season in the Upper Midwest is one factor likely weighing on green prices. Also, a producer in the Upper Midwest said some of the difficulty moving green Hard Maple might be related to limited kiln capacity for some drying operations.

SOFT MAPLE: Sawmills in the North are well supplied with Soft Maple logs and are expediting lumber production to prevent stain. The result is more price erosion this week. A producer in the Upper Midwest noted a particular oversupply of 8-foot Sap&Btr lumber. The green Fas&Sel listings fall across all thicknesses in both color designations. The green Unselected Fas&Sel listings have fallen for four straight weeks, while corresponding Sap&Btr listings have fallen for three straight weeks. All the published kiln dried figures hold steady following numerous drops last week. Sellers have noted that buyers are likely switching to Hard Maple, when possible, in order to reduce costs, another factor creating downward pressure on Soft Maple prices. One positive for producers is that brown Fas items are reportedly still in high demand.

RED OAK: Red Oak is moving well at firm prices for producers in the Northern region. A sawmiller in Minnesota told HMR/Fastmarkets that one of his regular buyers was “begging” him for a load of Red Oak, which he believes indicates that supplies are tight. Reported prices are maintaining a steady-to-firmer trend. Demand from the residential and truck trailer flooring sectors is most often described as “slow” by area contacts, so markets for green #2A&3A Red Oak are missing the typical seasonal boost from those sectors. All the green and kiln dried listings and ranges are unchanged this week amid largely consistent reported prices. The kiln dried net 4/4 Fas listing is up by 7% over the past four months.

WHITE OAK: White Oak prices maintain their downward trend this week, with further decreases in published green and kiln dried figures. The green #1C and #2A&3A listings fall across all thicknesses, along with all the kiln dried listings and most range numbers. Buying activity remains busier than during the first quarter, but the market is still characterized by oversupply that has persisted for roughly 18 months amid reduced consumption by the barrel stave sector. Producers able to offer relatively high percentages of longer boards or limited sapwood are sometimes obtaining price increases, but the market for random length lumber remains under downward pressure.

PALLET LUMBER, CANTS, TIES, & BOARD ROAD: The market for pallet lumber and cants is a bright spot for sawmill operators. Virtually every producer in the region has reported “good” demand and higher prices in recent weeks. No further increases are required for the listings and ranges this week following last week’s widespread gains.

Business conditions for railroad ties are slow. Treaters are maintaining strict purchasing quotas at steady prices for most suppliers. However, some producers in the Upper Midwest are receiving lower prices, leading to a slight drop to the low-end range number.

A wider range was discovered for board road prices, leading to an increase in the high-end range number. However, market fundamentals in that sector are steady, and the listing is unchanged.

Comments from June 19, 2026.

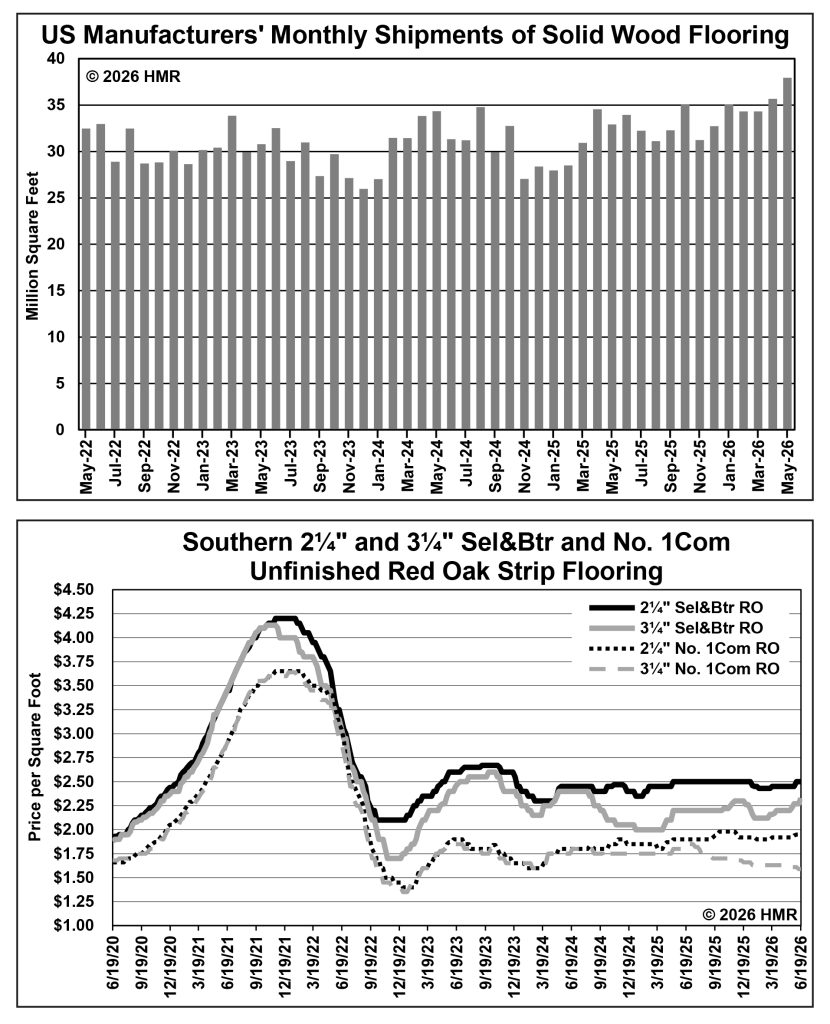

Illness and absenteeism kept Oak flooring production below desired levels in May at one plant. Severe lightning storms temporarily interrupted production at a second factory, while output at a third has remained low since it eliminated a shift in early spring.

While production slipped in May, factory shipment rose. US manufacturers’ shipments of solid wood flooring rose 6.4% in May from April, according to the final estimate by HMR/Fastmarkets, based on extensive industry surveys. One contact who reported low double-digit percentage growth in May shipments commented, “It finally feels like spring.” Elevated freight rates and booking cancellations by carriers hampered shipments at times, yet slightly more product shipped to distributors in May than April.

Ongoing price concessions are helping residential flooring plants move Sel&Btr White Oak flooring. Information lowers the listing for Southern 2¼” Sel&Btr White Oak and the associated range figures, while the only changes for 3¼” Sel&Btr White Oak lower both ends of the range. This week’s largest increase occurs to the Southern 3¼” Sel&Btr Red Oak listing. Reports also warrant gains to all 2¼” No. 1Com White Oak figures and an increase to the low-end range for 2¼” Sel&Btr Red Oak. Conversely, the Appalachian listing and the low end of the range for 2¼” No. 2Com White Oak decline. Finally, the Appalachian 3¼” No. 1Com Red Oak listing falls again.

Manufacturers generally aren’t comfortable enough with current market conditions to aggressively pursue flooring-grade lumber beyond short-term needs. Some plants have excess White Oak lumber inventories despite attempts to control receipts by offering below-market prices.

In some past summers, the combination of strong Oak flooring demand and concerns about raw material shortages prompted a rush of lumber purchases ahead of the July 4th holiday period. Some plants even accepted receipts 24/7 over the mid-year holiday while the hum of machinery inside plants was quiet. This, however, is not one of those summers. Many plants that only closed on July 4th in the past are taking the entire three-day holiday weekend off this year. Others are weighing decisions about taking extra days off to reduce lumber inventories and to prevent accumulating additional stocks of finished goods.

May 29, 2026